{kind=link}

The comparative insight is simple: if you need cash access now, not next billing cycle, the choice between a Didi Card cashback route and a conventional credit card rewards program matters. This article examines when each tool supplies liquidity, how to switch between them, and where the didi finanzas model fits into routine spending. The analysis focuses on practical trade-offs—cashback value, transaction timing, and payment rails—so you can decide with clarity rather than impulse.

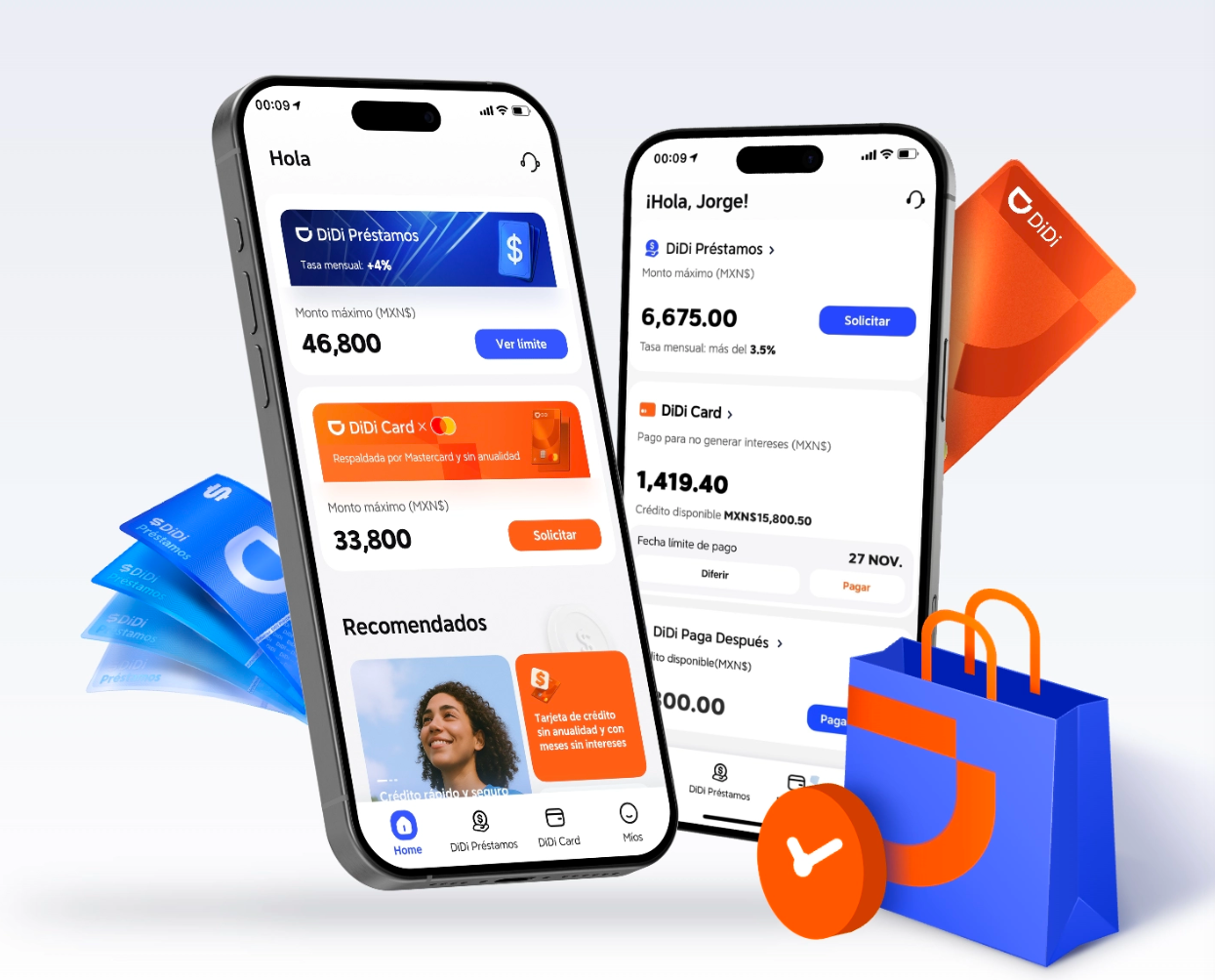

Mechanics at a glance: Didi Card cashback versus credit card rewards

Didi Card cashback typically posts rewards close to the transaction and sometimes lets users apply that credit instantly to a wallet or withdrawal. A credit card cashback or rewards program usually posts on the monthly statement and then offsets future balances or issues statement credits. Key terms to track: cashback rate, payment rails, and posting cadence. For users in dense urban markets—take Mexico City as an example—rapid credit to a wallet can translate into real, same-day liquidity for transport or small merchants. For clarity on how an integrated wallet behaves in practice, review the didi finanzas app features for wallet top-up and instant redemption.

When to favor Didi Card cashback for immediate liquidity

Choose Didi Card cashback when you need funds that clear quickly and you pay for goods or services that accept wallet or instant transfers. Didi-style cashback works well for recurring, low-value spend such as rides, food delivery, or convenience purchases where the cashback posts as a usable balance shortly after purchase. The trade-off is often a lower percentage reward than premium credit cards—but the speed of availability offsets that gap for short-term cash needs.

When credit card rewards win

Credit cards typically offer higher effective returns for larger or planned purchases through tiered rewards and sign-up bonuses. Use a credit card when you can pay the statement on time and when you value higher cashback percentages, travel points, or purchase protections. For liquidity beyond immediate needs, tools like balance transfer offers or short-term lines of credit can be more efficient—but they introduce interest risk and require discipline to avoid fees and carry charges.

Common mistakes and practical alternatives

Frequent errors are predictable: treating a cashback reward as identical to cashflow, delaying payment until rewards post, or carrying balances that erase any reward advantage. Alternatives include low-fee debit cashback cards, prepaid reloadable accounts, and selective use of buy-now-pay-later (BNPL) for planned purchases. Avoid using a rewards-driven credit card to cover living expenses that you cannot clear at statement; the net effect is negative once interest and interchange fees are considered. —A short note: mixing many reward platforms without tracking posting schedules creates dead money and frustration for users.

How to alternate them in practice

Operational steps to alternate effectively:

- Match payment method to desired outcome: instant wallet credit for same-day liquidity; credit card for deferred value and protections.

- Track posting cadence in a simple calendar or expense app so you know when cashback hits your balance and when the statement closes.

- Use small-value Didi-enabled purchases to seed a wallet, then reserve credit cards for larger transactions that need protections like purchase dispute or extended warranty.

Industry terms matter: cashback percentage, interchange, and APY (when comparing interest-bearing options). Monitor these to quantify trade-offs.

Three golden rules for choosing and measuring strategy

1) Liquidity window: measure how long between purchase and usable credit; shorter windows favor Didi Card routes. 2) Net benefit: calculate reward value minus any fees or interest—if carrying a balance, rewards rarely cover interest. 3) Acceptance and friction: prefer methods accepted by your frequent merchants and that avoid extra steps to redeem. Use these metrics to compare options consistently across months.

DiDi Finanzas offers a sensible bridge between immediate wallet credit and structured rewards—aligning liquidity needs with everyday spending. —Final thought: practical systems beat theoretical rates every time.