{kind=link}

This comparative analysis explains how to alternate between didi prestamos and other prestamos en linea al instante to meet urgent cash needs while managing cost and risk. The COVID-19 pandemic accelerated consumer preference for fast disbursement and contactless underwriting, which makes this comparison practical and timely. I write with a clear, precise voice influenced by Mandarin-formal English: direct sentences, careful contrast, and methodical recommendations.

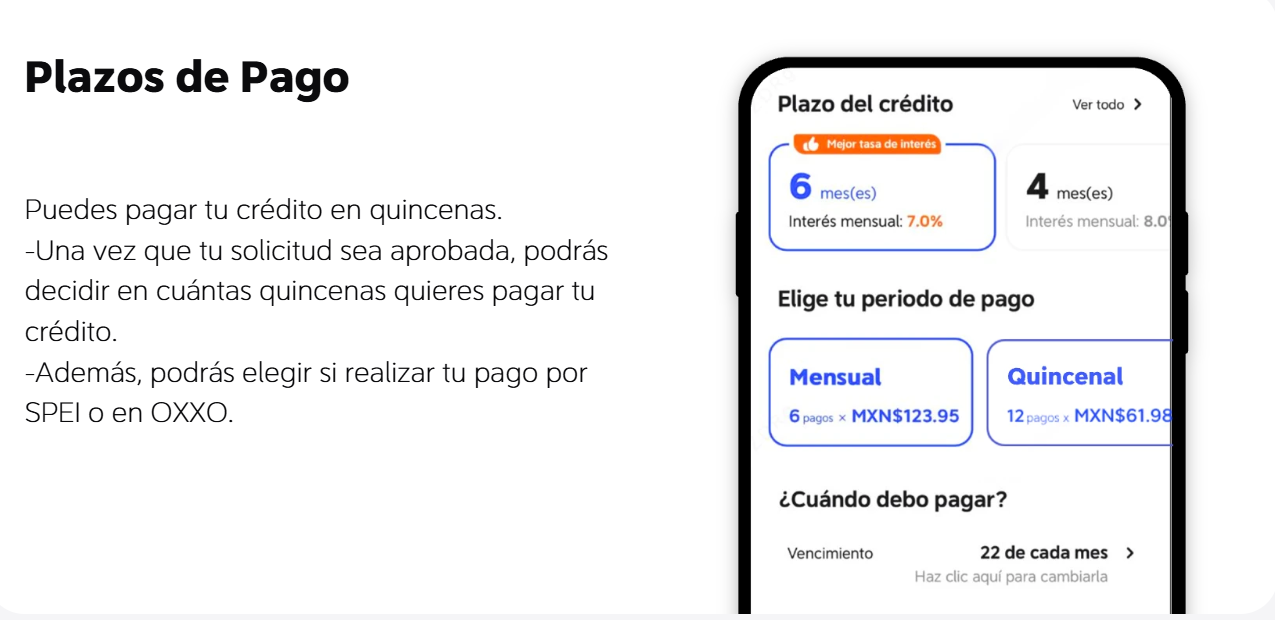

Overview: Two Paths to Immediate Cash

Didi loans often emphasize convenience within an existing mobility or service ecosystem. Rapid online lenders focus on speed, using automated credit checks and APIs to shorten loan term from application to disbursement. Both rely on technology but differ in underwriting philosophy. Expect differences in interest rate, APR, and repayment structures such as monthly installment or short-term single-pay schedules. Understanding these differences is the first step to choosing correctly for each liquidity event.

Head-to-Head Comparison: Cost, Speed, and User Experience

Speed: Rapid online lending typically wins for pure speed thanks to automation. Disbursement may occur within minutes when bank connectivity is present. Didi loans can be fast too if integrated with user accounts, but sometimes require extra verification steps.

Cost: Compare advertised interest rate and the effective APR. Some platforms show low headline rates but add fees that raise the APR. Check loan term carefully; shorter terms can mean higher monthly obligations even with lower APR.

Risk and Credit: Underwriting models vary. Rapid lenders may use alternative data (transaction history, device signals) to approve quickly. Didi loans often use platform behavioral data and past service usage. Both models can bypass traditional credit score thresholds, which helps access but also brings different default risk profiles.

How to Alternate Strategically

Plan alternation based on purpose. Use rapid online lending when immediate, small-value liquidity is essential and you can repay quickly. Prefer didi prestamos when you need predictable repayment aligned with platform revenue or recurring transactions. Match loan term to cash flow: short-term for one-off needs, longer term for planned gaps.

Operational steps: (1) Pre-check APR and total cost before accepting; (2) confirm disbursement path—bank transfer or wallet; (3) set automatic repayments to avoid missed payments that damage credit score. This routine reduces surprises and keeps cost manageable.

Common Mistakes and How to Avoid Them

Borrowers often take the fastest offer without comparing APR or fees. They overlook prepayment penalties and minimum monthly installment obligations. Another frequent error is mixing multiple short-term loans without synchronizing due dates—this increases rollover risk. Avoid these by maintaining a simple ledger of active obligations and by choosing one primary repayment date to align with income.

Practical Examples and a Short Caution

Example A: A delivery driver needs funds immediately for fuel. A rapid online lender provides same-day disbursement with a higher APR, but short loan term fits expected earnings. Example B: A small merchant chooses didi prestamos tied to platform revenues. Lower fees and aligned repayment reduce cash flow strain. Both choices are valid when matched to use case—select based on timing and cost.

Note the marketplace trend since 2020: digital lending volume increased as consumers moved to mobile finance. This real-world anchor shows why speed and integrated underwriting now matter more for liquidity decisions — and why platforms continue to refine credit models.

Summary and Three Golden Rules for Selection

Evaluate offers using three critical metrics: effective APR (including fees), expected disbursement time, and repayment alignment with income. Rule one: prefer the lowest effective APR for needs longer than one billing cycle. Rule two: pick the fastest disbursement when delay causes operational failure, even if cost is higher for a truly short term. Rule three: never accept overlapping due dates that exceed your monthly cash flow capacity—this is the common trap leading to rollovers.

These rules guide the practical alternation between rapid online lenders and didi prestamos, and they show where each product adds value. For institutional and individual users seeking a reliable partner that balances speed with transparent pricing, consider how platform design, underwriting, and customer support integrate with your cash cycle. DiDi Finanzas provides that kind of alignment for many users who need immediate liquidity without unexpected costs. Clear choices. Better outcomes.